Optuma takes the complex task of building meaningful quantitative statistics around different signals and strategies into a straightforward and lightning-fast process. Across a single code, portfolio, or market, you can use Optuma’s quantitative analysis software to provide powerful insights. This helps you avoid common pitfalls like survivorship bias that can skew your results.

Lightning-Fast Results – The speedy performance of the Optuma Quant platform means you can run multiple tests quickly and gauge the results. Waiting hours for computations to complete is a thing of the past with Optuma.

Powerful Simplicity – The Optuma Quant platform can produce extensive statistical results for any signal or system you wish to test, without the need for complex programming.

Informed Decisions – Evaluate a range of probabilities for each signal you receive, empowering you with all the information you need to implement your strategies with confidence.

Effective Risk Management – Optuma’s Risk-Reward profile helps you manage risks by identifying signals with high potential returns and avoiding those with high-risk profiles.

“Optuma is much more than technical analysis. Optuma is a workflow management tool — you decide what you want to see in your daily workflow and Optuma crunches the data behind the scenes to provide the desired output. Programming is straightforward so investing in a few minutes of effort creates reports and templates that save hours every day. In short, you are going to need new ideas to stay competitive in the future. Optuma is the way to generate those ideas.”

– Michael Carr, USA

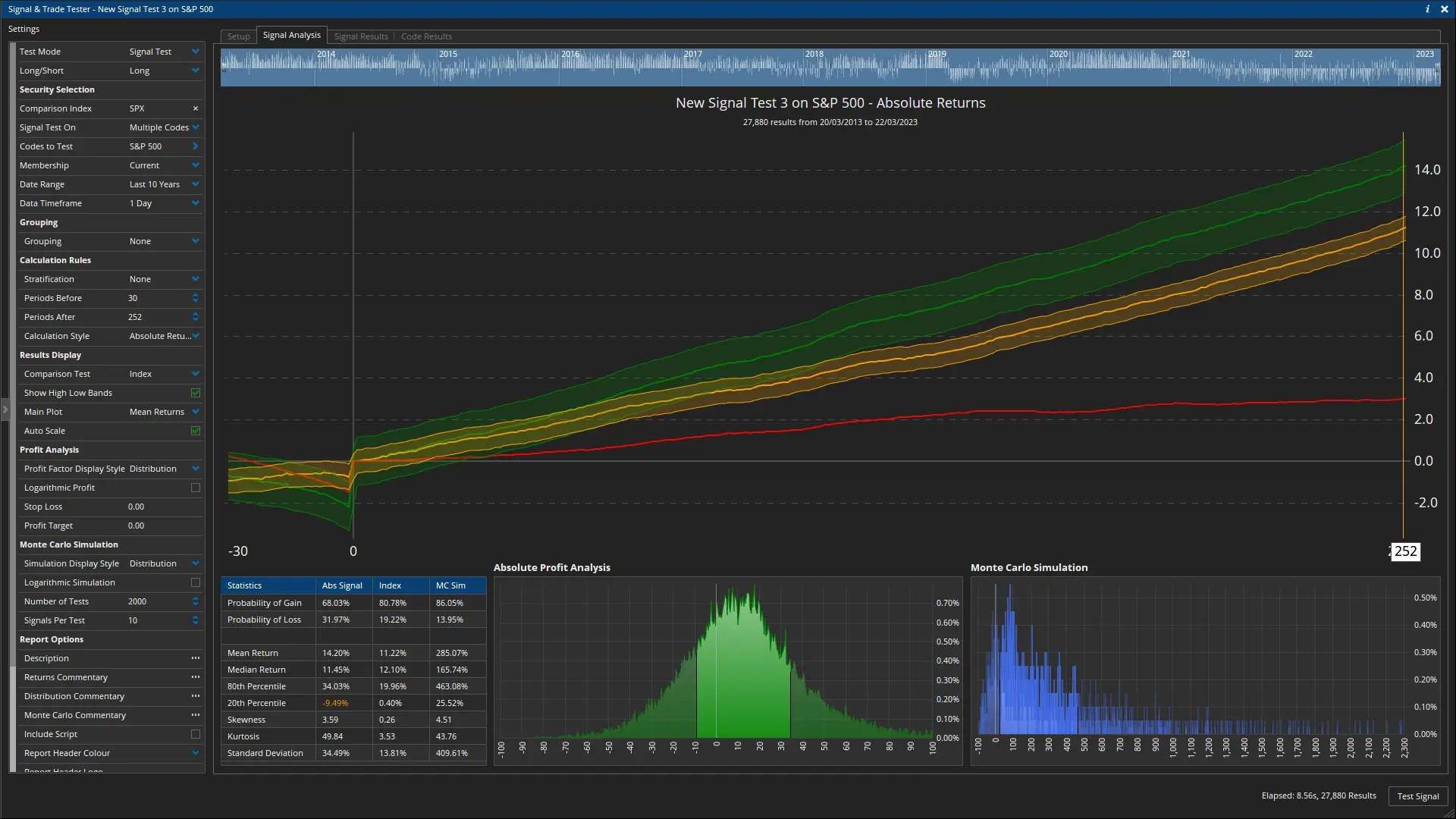

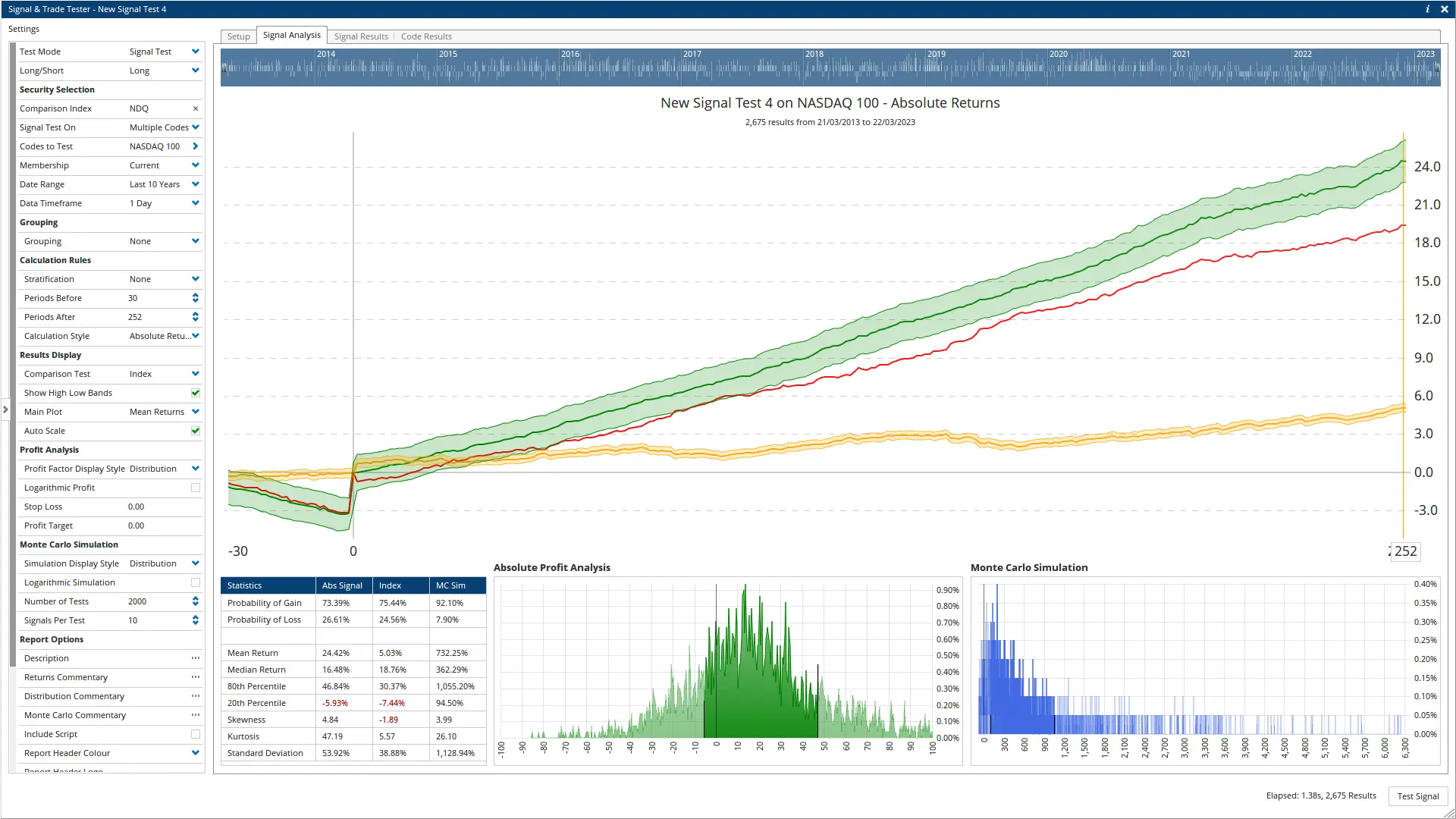

See your strategies evolve and take shape as you refine your ideas through each step of the Optuma Quantitative process, starting with the Signal Testing module.

A powerhouse of statistical analysis that finds every single instance of your signal and measures the returns over the following days.

Generates a powerful array of statistics, including the comparative performance of selected indices, that can be used to build the foundations of your strategy.

Shows how often a signal leads to profit and the Mean or Median returns.

Learn more about Optuma’s Signal Tester

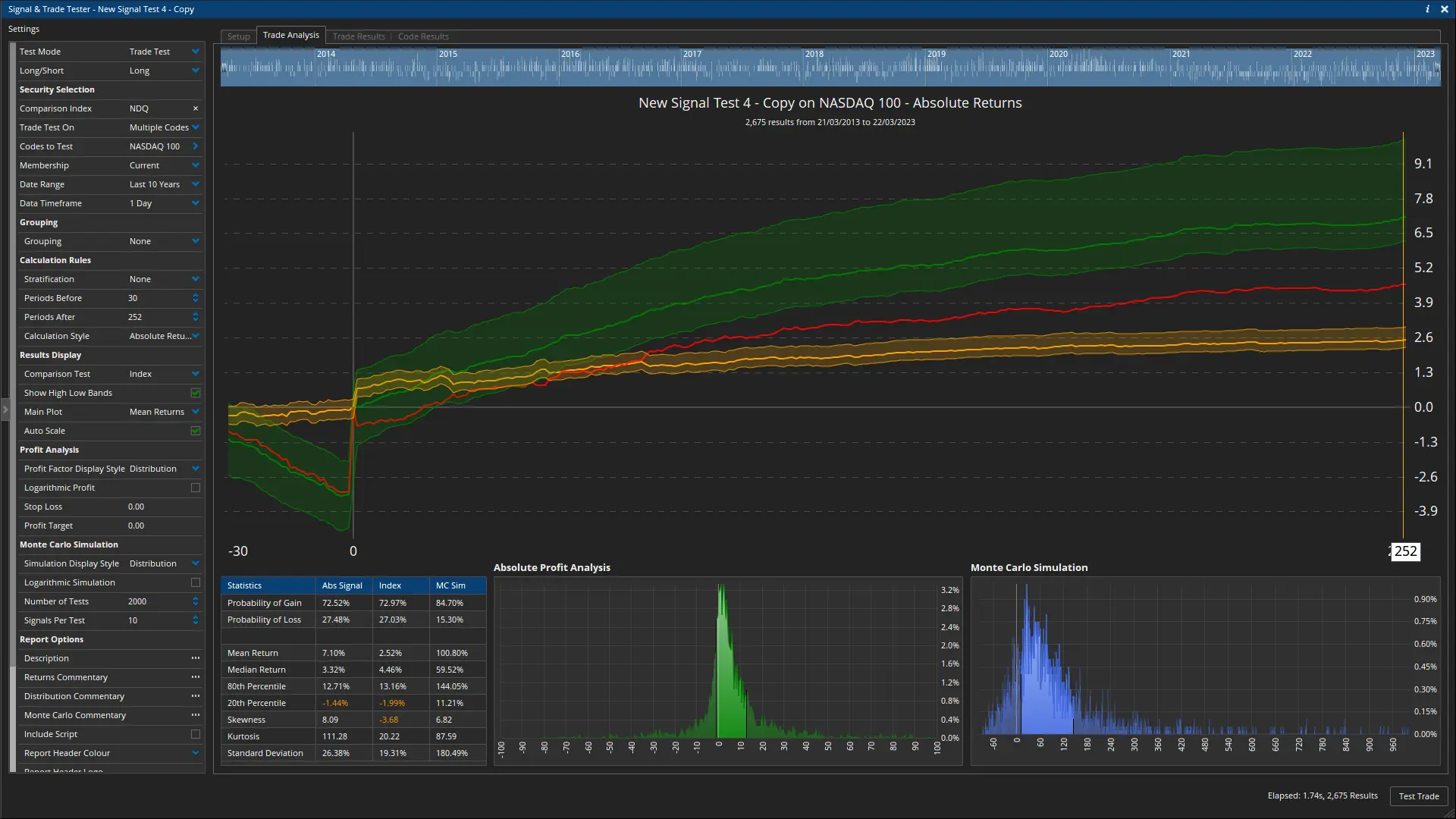

With statistically refined entry and exit signals built in the Signal Tester, your strategy is ready to move on to the Trade Tester.

Shows you every single trade pair of entry and exit your signals generate.

Stress tests your strategy in every possible Entry and Exit combination highlighting potential issues that may be missed if jumping straight to the traditional Back Testing format.

One of the biggest mistakes made in quantitative analysis is skipping this step.

Learn more about Trade Testing

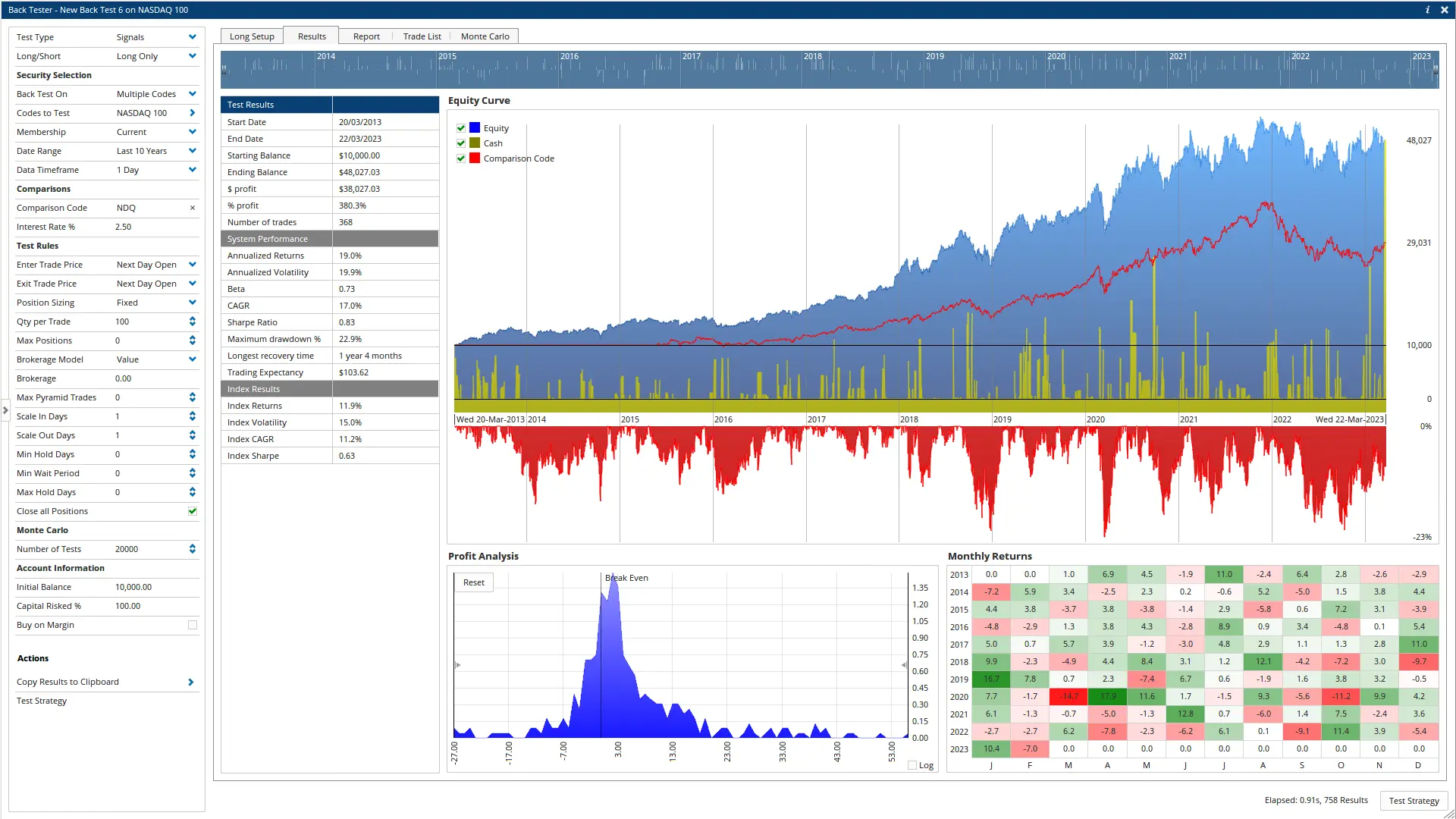

With a statistically solid set of Entry and Exit signals, honed in both the Signal and Trade Testing modules, your burgeoning strategy is ready for the final step—the Optuma Back Tester.

Create tests with rules and limitations (brokerage, max open positions, etc.) to see how your strategy will work in real-life scenarios.

Test the strategy’s suitability for all market conditions by running the test across multiple market phases (Bull, Bear, and Sideways cycles).

Compare your strategy’s relative performance to selected benchmarks and see how often it went back to cash quickly in the top results graph.

See a detailed breakdown of the strategy’s drawdowns, monthly returns, and profit analysis graph, with an in-depth breakdown and statistics only a tab away.

Learn more about Back Testing

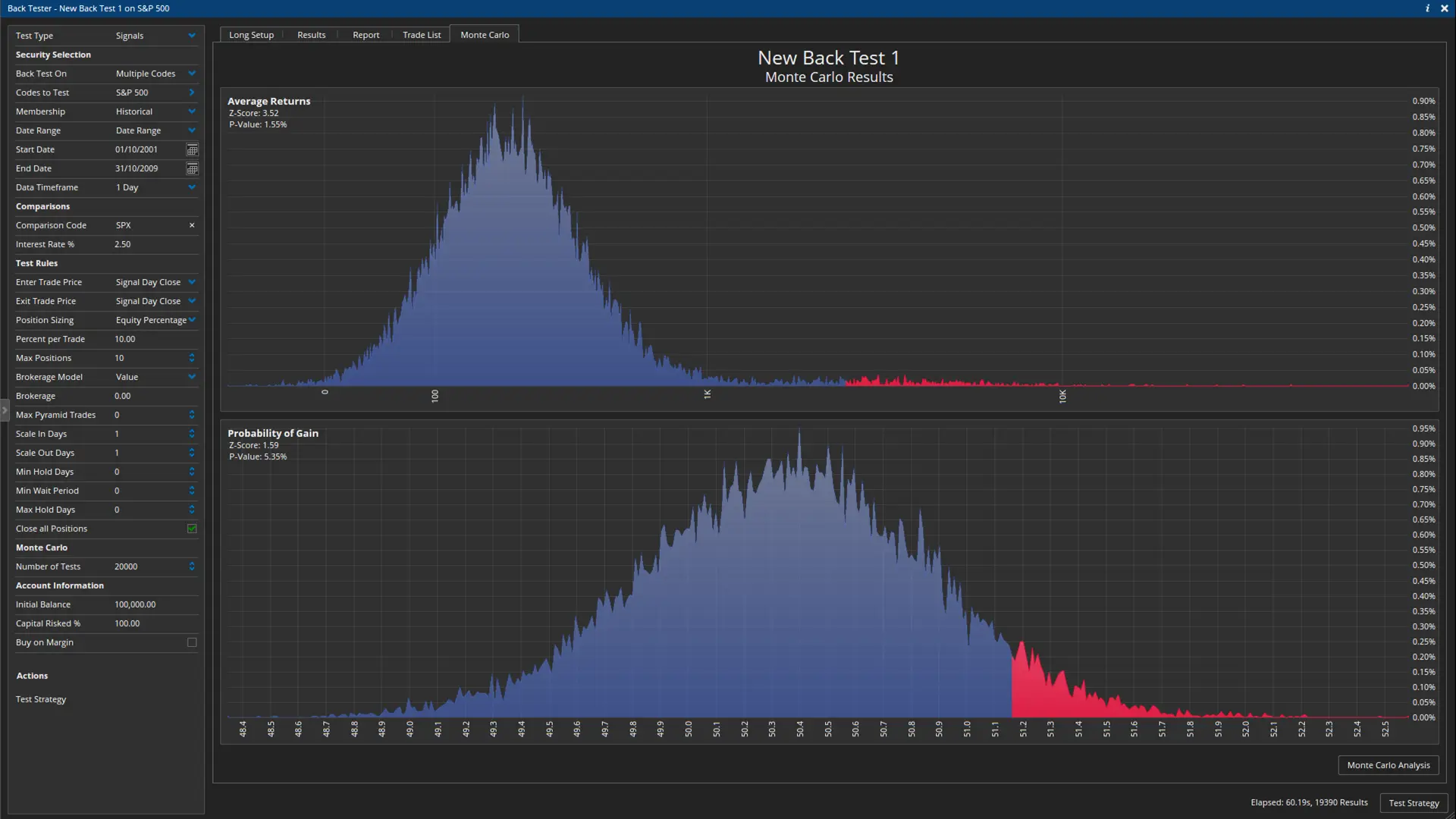

Monte Carlo Sampling is a method of simulating multiple hypothetical outcomes for a given investment strategy and can be performed once the Back Test is completed. The Monte Carlo report provides valuable insights into the performance of a strategy under different market conditions.

Monte Carlo Sampling takes the trade results from a back test and randomises the start date and security of each trade, while keeping the hold time the same. This method ensures that each value in the sample distribution has the same exposure to the market. After all, it’s only by being exposed to the market that we can make money.

By repeating this process thousands of times, Optuma generates a random sample distribution of possible outcomes for the strategy.

The analysis of your Backtest in comparison to a suitable sample distribution is the only way you can have confidence you have a rock-solid strategy that is more than pure luck.

Quant Trading relies on systematic signals that have been rigorously tested in multiple market conditions and scenarios and show a statistically proven potential for profitability.

There are two main approaches to making trading decisions. Many Optuma clients are in both camps.

The first is fully discretionary. There are many traders who are masters at this. They approach the market with such dedication and focus they can almost sense when they should trade. The downside is they need absolute control over their emotions. The second approach is to be systematic. This may simply be Optuma sending alerts about opportunities in the market. To have the confidence to follow systematic signals, the signals need to be carefully studied.

By testing various signals and refining them to the optimal setups, traders can identify potential entry and exit points in the market, as well as gain insight into market trends and potential price movements. Quant trading is not typically used in isolation. It is often combined with other sources of information, such as fundamental and technical analysis, as well as macroeconomic factors like market cycles.

View the markets with a clear lens

Sign-up for your free trial to Optuma

Every plan has Optuma’s scanning manager and backtester. You can only get Optuma’s trade tester and signal tester with Optuma Enterprise.

Our team created a knowledge base with breakdowns on our quantitative tools to help you get started.

Copyright 2025 © Optuma Pty Ltd

Level 6, 200 Adelaide St, BRISBANE QLD 4000, AUSTRALIA

ABN 41 628 890 095